Working out rehab costs can feel like solving a riddle. Insurance paperwork, random fees, and all sorts of fine print seem to get in the way of finding a straight answer. I’ve spent a lot of time sorting through these details, so here’s my plain-English guide to what really goes into the price of addiction rehab, plus what your insurance company might not lay out clearly.

How Rehab Costs Break Down: Sneaky Fees and Overlooked Expenses

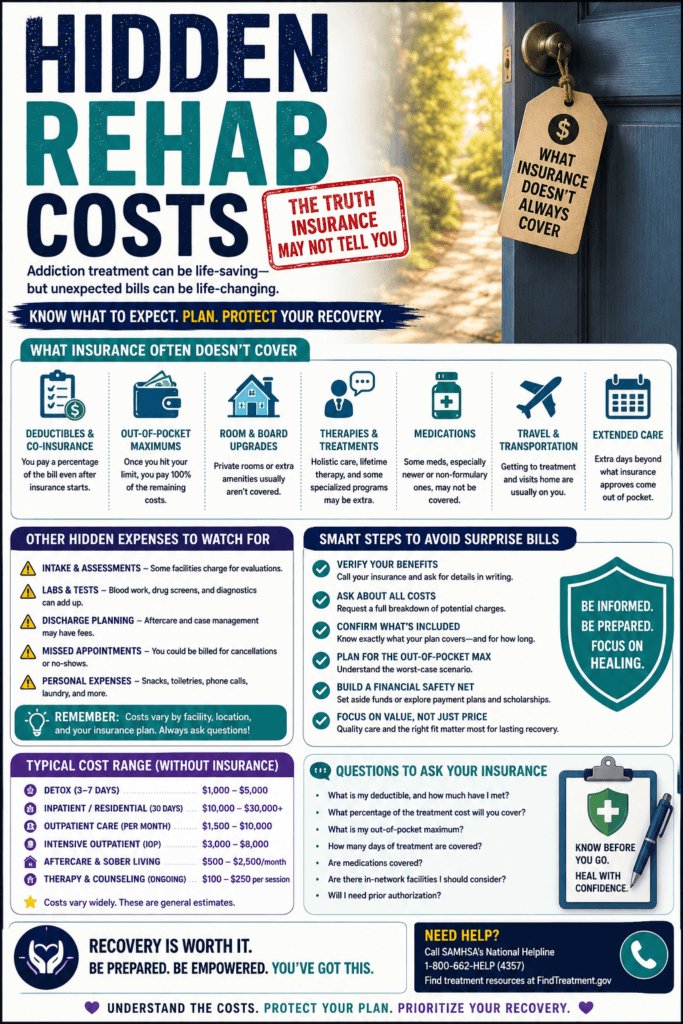

For many people, sticker shock hits hard when they first see the total price of a rehab program. It’s easy to assume insurance swoops in to cover it all, but the reality is a bit messier. Rehab programs usually bill you for a mix of things: medical treatment, therapy, accommodations, meals, and extra services. Each of these adds to the final bill, and not all of it is obvious upfront.

Residential (inpatient) rehab is usually the priciest, mostly because you’re paying for 24/7 care, a room, and meals. Outpatient options tend to cost less because you go home at night. But what really throws a wrench in the budget are a few “hidden” insurance costs that don’t advertise themselves, like admission fees, detox add-ons, or surprise lab work. Even when initial costs seem clear, hotels and treatment amenities may incur upcharges that only appear on the final bill.

The Insurance Game: What Gets Left Out

Insurance plans love to talk about mental health coverage, but the details can get a little fuzzy. Most policies mention they cover addiction treatment, but they don’t always say how much, for how long, or exactly what’s included. Sometimes, only the basics like doctor visits or certain medications are covered, while you’re left holding the bag for counseling sessions, holistic therapies, or extended residential stays.

Some common insurance surprises I’ve seen include:

- High Deductibles: Even if rehab is “covered,” you might have to pay several thousand dollars before insurance gets involved.

- Co-Pays and Coinsurance: Each session or day of treatment may be subject to a set fee or a percentage of the total cost.

- Pre-Authorization Hurdles: Insurers typically require you to complete paperwork or obtain referrals before they approve coverage.

- Out-of-Network Fees: If the rehab center isn’t in your insurer’s network, you could be on the hook for most or all of the bill.

Before admission, it helps to call your insurance company and ask for an exact breakdown of what’s covered, what isn’t, and what you’re on the line for. This can help you avoid sudden costs after discharge.

Different Rehab Types and How Costs Add Up

Rehab isn’t one-size-fits-all, and costs vary by program type. Here’s how the main categories play out:

- Inpatient Rehab: This option is usually the most expensive. You’re basically paying for room and board, constant supervision, medical support, and full programming. Prices can range from $6,000 to $30,000 for a month, depending on the center’s amenities and location. Some even surpass that bracket, especially in destination settings.

- Outpatient Rehab: This lets you live at home while attending therapy sessions. Outpatient rehab can cost anywhere from $1,000 to $10,000 for several months, and it’s more likely to be partly covered by insurance.

- Detox: Some programs require a separate detox period before you’re admitted to the rehab center, which is a separate charge. Detox alone often costs $300 to $1,500 per day, and sometimes insurance will only cover a set period or a few days.

- Luxury or Executive Rehab: These centers resemble resorts and offer perks such as private suites, gourmet meals, and spa-like settings. These extras don’t always mean better clinical care, but they can double or even triple standard prices.

Every choice affects what you’ll pay, so it’s worth comparing types and asking what each line item means before signing on. Sometimes, even transportation to and from the facility is billed separately, depending on what’s included.

Decoding the Fine Print: Coverage Limitations You Might Miss

Insurance fine print can trip up even the most prepared folks. There’s a big difference between “rehab is covered” and “all expenses are paid.” Some of the most common gotchas include:

- Limits on Time: Policies sometimes cover only a set number of days or sessions. If you need more time, you could be on your own for the bill.

- Type of Therapy: Individual talk therapy may be covered, but family sessions, group activities, or special wellness classes, such as yoga or art therapy, may not be.

- Medication: Some insurance plans skip newer medications or require you to try cheaper alternatives before covering brand-name medications (a process called step therapy).

- Facility Requirements: Only rehab centers certified or accredited by certain organizations are eligible for coverage under most insurance policies.

Always double-check which therapies, medications, and lengths of stay are actually included, especially if you want to avoid surprise bills. Reading the plan documents closely or talking with a dedicated insurance specialist at your rehab center can save you a huge headache later. Even services as basic as follow-up medical checks can slip through the cracks.

Upfront Vs. Extra Costs: What Isn’t Always Obvious

I’ve worked with plenty of folks who thought their rehab package was “all-inclusive.” Then they saw a bill for things like:

- Initial Assessments or Intake Fees: Some centers charge an upfront fee just to process paperwork and set up a care plan.

- Lab Tests: Bloodwork, drug screenings, or medical checks can be billed separately, especially if not directly tied to the main treatment.

- Aftercare Planning: Support after you finish residential rehab, such as ongoing counseling or sober living, often isn’t covered by insurance plans.

- Special Amenities: Massages, nutritional counseling, fitness training, and similar “extras” are usually not covered and can be surprisingly pricey.

Asking for a full, itemized cost estimate before you start rehab can save a lot of stress and confusion. Reputable centers are usually happy to break everything down for you. If you’re unsure, don’t hesitate to get these costs clarified in advance.

What To Ask Your Insurance Provider Before Starting Rehab

Getting someone on the phone from your insurance company can feel tricky, but it’s a good idea to have your questions written down ahead of time. Here are a few worth asking directly:

- How much of inpatient and outpatient rehab will you cover in dollars and days?

- What’s my deductible, copay, or coinsurance for addiction treatment?

- Are there any specific rehab centers or therapists I should choose from?

- Is detox covered, and for how long?

- Are special amenities like fitness or art therapy included or excluded?

- What about aftercare—will you help pay for follow-up counseling?

You might need to ask for these answers in writing, so you have proof of coverage details if there’s a billing mix-up later. Don’t be afraid to go over details more than once until you’re confident in the numbers.

Tips for Reducing Out-of-Pocket Rehab Expenses

While insurance can help ease the burden, I still see many people scrambling to cover what’s left over. A couple of things can help bring the numbers down:

- Comparison Shop: Prices and insurance acceptance can vary widely from one center to the next. Calling two or three places can help you find the best fit for your budget.

- Ask About Sliding Scales or Payment Plans: Some facilities work with your finances for monthly installments or charge less for lower-income clients.

- Look into State or Nonprofit Help: Many states offer public funding or scholarships, especially for first-time treatment seekers.

- Consider Outpatient Options: If your situation allows, outpatient rehab can be just as effective for many people and much easier on your wallet.

- Double-check Network Status: Using an in-network facility almost always slices your bill down to size compared to an out-of-network one.

With a little planning, the need for high-quality care doesn’t have to mean total financial upheaval. Don’t hesitate to ask about costs up front and look into grants or payment assistance if money is tight.

Real Life Example: Josh’s Experience with Unexpected Costs

To put these ideas into perspective, Josh, a friend of mine, thought his insurance would pay for the bulk of his monthlong rehab. He found a rehab that accepted his insurance, verified coverage, and went in thinking he’d just owe a low copay. Three weeks later, he got a $2,800 bill. Turns out, his insurance capped coverage at 14 days, didn’t pay for group therapy, and the detox was billed separately. Josh’s situation made me realize how important it is to pin down the details before checking in. Getting the right information saved him from even bigger financial surprises.

FAQs About Rehab Costs and Insurance Surprises

Question: Will insurance always pay for rehab?

Answer: Not always. Some plans cover only certain types of rehab, limit the number of days they’ll pay for, or include only specific providers. Always verify directly before starting treatment.

Question: Is detox included in the standard rehab cost?

Answer: Not always. Detox can be a separate charge, even if it happens at the same facility. Insurance might handle detox and rehab as separate benefits, so ask for details about both.

Question: Are there programs for people with little or no insurance?

Answer: Yes. State-run centers, public grants, and some faith-based or nonprofit rehabs offer low-cost or free options, though availability varies by location.

Final Thoughts

I know rehab pricing can feel intimidating, especially with so many moving pieces and hidden costs insurance doesn’t spell out. Careful research helps buyers make informed decisions and reduces the risk of an expensive surprise. Asking direct questions, reading the fine print before signing anything, and making sure you know exactly what’s being billed can make the whole process smoother. When health and peace of mind are at stake, having clear info on your side is super important. If you take time to ask questions up front and look at the details, you can focus on recovery instead of stressing over bills.

Video: This is Why People Can’t Afford to Get Help #addiction #reality #treatment